| Frequently Asked Questions |

|

|

- Why is Credit important ?

Credit is a financial tool that enables you to buy things now without paying for them all at once. Your ability to use credit responsibly and repay creditors on time has a lot to do with how much access to credit you will have in the future. Building a solid credit history gives you more buying power when you need it, and that can be especially valuable when you are buying a high value product or service.

Back to Top

- How Does The Process of Credit Repair Work?

The credit bureaus, as well as creditors, are required to follow accuracy procedures before they can legally place information on your credit report. Any information that is not complete, or not accurate, or not verifiable is not supposed to remain. During the process we force the creditors and credit bureaus to back up their claims of accuracy. Once an error is identified, if it can't be proven 100% accurate, the item must be removed.

There are other methods also used in special situations. These are explained on a case-by-case basis.

We start by examining our client's personal credit file held by each of the major credit reporting bureaus (TransUnion, Equifax and Experian). Then, we identify any accounts that contain information that could be considered adverse.

Next, upon the client's request, we dispute all of the accounts that contain inaccurate, erroneous, or obsolete information on the client's behalf and have the accounts deleted or updated accordingly. Finally we consult our clients on how to avoid future negative credit listings while educating them with helpful tips on how to use their credit to their advantage and boost their scores.

Back to Top

- How Will I Know When The Negatives Come Off My Reports?

You will receive an update from the credit bureaus themselves for each issue that we initiate an action on.

Back to Top

- How Long Will The Whole Process Take?

In the vast majority of cases, our clients see results in as little as 60 days. The length of time to complete the full program will vary from client to client. Each case is unique. The number of issues, the type of issues, and the participation level of the creditors and bureaus will all have an impact on the speed of the process. Typically, the range will be from 6-10 months. You can help insure the fastest process with timely participation when necessary.

Back to Top

- What if I don't hear from the credit bureau?

If two weeks go by and you don't hear anything from the credit bureau please contact us. Sometimes the credit bureaus don't get your letter request, and sometimes they just want to ignore you.

Back to Top

- What if some of the credit collectors call me?

Tell them to send you a copy of a contract with your signature stating you owe them the stated money. The collection agency can't collect from you without a signed contract. The best thing to do is not talk to them at all.

Back to Top

- What is the Federal Credit Reporting Act?

The FCRA : your right to accurate credit reporting.

The Fair Credit Reporting Act (FCRA) was enacted in 1970 to promote fairness, accuracy and the privacy of personal information reported to credit bureaus by creditors and others.

The FCRA allows a consumer to challenge the information on his or her credit report on the basis of "completeness and accuracy."

The credit bureaus are required to complete the investigation within a "reasonable period of time." This time period has been set at thirty days.

If, after an investigation by the credit bureau, the disputed information "is found to be inaccurate or can no longer be verified, the [credit bureau] shall promptly delete such information."

In theory, the disputation process should be simple, but many consumers quickly discover that exploitative creditors and abusive debt collectors can make the process more difficult than they imagined.

Creditors routinely charge higher rates of interest to those with negative credit histories, so sloppy credit reporting may serve to maximize their profits, a circumstance that can make the process of credit repair a difficult and frustrating experience for most consumers.

Back to Top

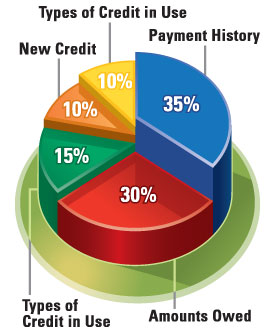

- Payment history: 35 percent.

The single most important thing you can do is the simplest: Pay your bills on time. More than a third if your FICO score is based on your payment history: how often you're late paying credit cards, car loans, mortgages and student loans. The later you are, the more you hurt your score. And closing an account with late payments after you've paid it off doesn't get rid of the damage to your score any faster than leaving it open.

Back to Top

- How much you owe: 30 percent balance owed.

The next biggest chunk of the score is based on how much you owe. The simplest solution: Pay down your credit cards and other installment loans. Moving money from one card to another won't help: you have to reduce the overall balance.

Credit issuers also look at how much of your borrowing power you're using. Even though you're keeping up with monthly minimum payments, if you're at your limit on one or more cards, you're at greater risk of getting in over your head ? which will likely be reflected in your score. On the other hand, if you can get your bank to raise your limit, the extra headroom on your account should help your score.

Back to Top

- Length of credit history: 15 percent.

This one is hard to speed up; lenders want to see a track record of timely payments. Even if you have had credit for along time, a lot of newer accounts will lower your score. That's why closing old accounts may reduce your score: it may shortens the average length of your credit history.

If you're just getting started, stick with one or two accounts and gradually add more. If you can get yourself added to an account of a relative with good credit, that may help. And if you have no credit history, you may want to start with a secured loan or credit card. By keeping money in a savings account with the same lender ? and using it to back your loan ? you'll lower the risk to the lender, get a better rate and start building a good payment history.

Back to Top

- New credit: 10 percent.

Opening up a lot of accounts all at once can also hurt your score ? even if you pay all your bills on time and don't carry big balances.

You may also hurt your score if you're constantly changing cards and chasing a lower rate. Your score can also take into account how many inquiries lenders make to credit agencies asking about your credit. Too many request for information may mean you're embarking on a borrowing binge. On the other hand, Fair Isaac says it doesn't count inquiries form lenders who want to pre-approve you ? without your approval. And shopping among several lenders all at once - without opening more than one account ? also shouldn't have an impact, according to the company's Web site.

Back to Top

|

|

|

|  |

|

|

|

|

|

|

|

|

The Credit Repair Organizations Act

This act spells out the obligations that credit repair organizations have when providing services to consumers. There are many rules that these companies are obliged to follow, and they are designed to protect the consumer from credit repair scams and unreasonable offers. Some important details are outlined below. Credit repair companies are legally required to:

- Provide a copy of the "Consumer Credit File Rights Under State and Federal Law" prior to an individual signing any contract with them.

- Provide a written contract that clearly spells out your rights and obligations.

- Read these documents carefully and understand their contents fully before signing the contract.

As well, credit repair companies cannot:

- Make false claims about their abilities, qualifications or services.

- Provide their services until after an individual has signed their written contract.

- Complete any services until after the three day waiting period AFTER the signing of the written contract has expired

Any contract an individual signs with a credit repair company must include:

- All payment terms, including a total cost for all services.

- Expected length of time that will be required to achieve results.

- Concise description of the services to be given.

- Any and all guarantees they offer

- The credit repair company's name

- The credit repair company's address

|

|